Company Benefits

Mission Statement

Mission Statement

The mission of EverGRO FS is to be a financially strong and progressive agricultural cooperative, that enables our customers and patron owners to be successful, profitable, and sustainable through excellent service and competitive values.

We want to highlight the following benefits for our full-time eligible employees. This guide will provide an overview of the benefits full-time employees are eligible to participate and utilize. We recognize that competitive and value-adding benefits are an important component to our employee’s overall fulfillment in their careers and we hope our benefits will add value to your experience with EverGRO FS.

Each year we are dedicated to reviewing our benefits and evaluating our options. In addition, each year we will offer an Open Enrollment period for all employees to have the opportunity to review and change their benefits for the upcoming year.

This Enrollment Guide provides you with a general overview of the benefits offered to you. It is important that you familiarize yourself with the benefits EverGRO FS offers from the information provided in this booklet. We encourage employees to review the more comprehensive and detailed resources provided by our carriers.

You will be provided a comprehensive booklet from our providers:

- Sentara: Medical

- Anthem: Dental and Vision

- Mutual of Omaha: Group Life with AD&D, Disability, Critical Illness, Accident, Voluntary Life, Employee Assistance Program, & additional discounts and services.

Dependents / Beneficiaries

Dependents / Beneficiaries

When enrolling for your benefits, you will be able to select and identify your dependents and beneficiaries. Please make sure to have their personal information ready to enter into the system, i.e. date of birth, social security number, etc.

Additional Resources

If you have specific questions please direct them to the Human Resources department. You can also visit our providers website or call for additional questions related to coverage, specific plan details, in-network providers and more.

Enrollment Instructions

Benefit Enrollment will be offered through our vendor, Employee Navigator. Benefit enrollment must be completed virtually by visiting their website at, www.employeenavigator.com. Instructions will be provided to each employee on how to login, create a new user account and get started. Employees can login to review their benefits 24/7. During our annual open enrollment, the company will specify the timeframe when this resource will be available to complete.

You have 14 calendar days from the start of employment to enroll in your benefits. They will then take effect the first of the month following your start date.

*Exceptions to this could include annual open enrollment period or a life changing event during the year.*

Payroll Deductions

You pay for your share of your benefit costs through payroll deductions. Deductions are equally divided by EverGRO FS’ 26 pay periods. It is your responsibility to verify that the benefits elected were applied and premiums deducted properly from your first paycheck in January or on

your first applicable paycheck following your start date.

You will pay for Medical, Dental, Vision, FSA, and HSA with pre-taxed dollars and Supplemental Life, Spouse Life, Child Life, AD&D and all of the Voluntary benefits with post-tax dollars.

Who Can Enroll in Benefits

All full-time EverGRO FS employees are eligible for our benefits. For details regarding who is eligible to enroll in benefits, review the specific plan descriptions from our providers, Sentara, Anthem, and Mutual of Omaha.

Benefit Options

BENEFITS OFFERED

EverGRO FS will offer the following benefits to eligible employees, which include, but not limited to the following options highlighted in this guide:

- Medical

- Dental

- Vision

- Life: Voluntary and Group and Accident Death and Dismemberment

- Disability: Short-Term and Long-Term

- Critical Illness Insurance

- Accident Insurance

- Flexible Spending Accounts: Personal Health Care Spending Account, Dependent Care Spending Account, Limited Purpose Spending Account

- Paid Time Off

- EverGRO FS Employee Discounts & Perks

- Retirement Savings Plan

- Employee Assistance Program

ADDITIONAL BENEFITS

EverGRO FS also offers additional benefits for full-time eligible employees that are not specifically outlined in this guide, but more information can be found by contacting your supervisor or HR.

Other benefits include but are not limited to the following and are applicable based upon position:

- Employee Referral Bonuses

- Cell Phone Reimbursement

- Mileage Reimbursement

- Company Issued Vehicles

- Company Issued Cell Phones & Laptops

Medical Plans Information

EverGRO FS’ medical plan advisor is Sentara. There are three medical plans, with 5 enrollment classifications to elect from; employee only, employee + spouse, employee + child, employee + children or family coverage.

Medical Terms Described

PREMIUM

The premium of a plan refers to the amount that will be deducted from an employee’s paycheck as outlined. In many cases in this guide, the premiums are listed according to a bi-weekly payroll period. This is also sometimes referred to as the “employee contributions.” Premiums will vary based on the medical plan.

DEDUCTIBLE

The deductible of a plan is the set amount you pay each year for covered services before your plan starts to pay for covered health care costs. There are different deductible levels for individuals versus employee + child(ren)/family. You can use your Health Savings Account or Flexible Spending Account funds towards your deductible. Deductibles will vary based on the medical plan.

CO-PAY

A flat fee you pay for covered services, such as a doctor’s visit.

COINSURANCE

Once you have met your deductible, the coinsurance is what you and your health plan share the cost of for covered health care services. You will see this listed in the chart following by the percentage (%) AD (after deductible). Therefore, the percentage listed, if there is one, would be the percentage the employee would be responsible for paying of the health care costs; while the remaining percentage is covered by the health care provider. For example, look at the HSA ($3,300) Embedded plan, if an employee meets their deductible (and it’s employee only coverage), if they go to the doctor again and their visit was $100, they would be responsible to pay 0% AD. Therefore, the employee wouldn’t pay anything more.

ANNUAL OUT-OF-POCKET LIMIT (MAXIMUM)

This is the most you have to pay out of your own pocket each year for covered health care services. This amount may include your

deductible and your co-pays and coinsurance payments, depending on the plan. There may be plans that still have you pay a copay at the time of service.

EMBEDDED

If you enroll anything beyond employee only coverage, the individual deductible is embedded in the family deductible. The term embedded means that each covered member of your family could satisfy an individual deductible without the family deductible being met. Once a family member meets the individual deductible, the plan will pay any future medical expenses based on the policy for that member only. The family deductible would need to be met by the remaining family members to have medical bills paid for those members.

For example, if you, your spouse and child enroll in the HSA ($3,300) family coverage and your child incurs $3,500 in medical bills because the deductible for that plan is $3,300 for individual, your child would meet their deductible and therefore, any subsequent medical bills for the child that year would be covered based on the plan guidelines, even though the family deductible of $6,600 has not been met yet. Once the family deductible is met, you no longer have to meet an individual deductible.

NON-EMBEDDED

If you are enrolled in anything beyond employee only, the plan then only contains a family deductible. There is not an individual deductible embedded in the family deductible. In this situation, the entire amount of the family deductible must be met first before the plan pays a portion of the cost of your medical bills. It can be met by one family member or a combination of family members. There are no benefits paid until expenses equal the full family deductible amount.

Medical Plans Summaries

Below is a brief overview of the three (3) medical plans employees are able to enroll. For additional details on any of the medical plans, we encourage employees to review the detailed guides provided to you from Sentara.

Sentara $1,000 POS

The Sentara $1,000 POS plan mirrors the characteristics of a PPO plan. This plan provides the highest level of benefits when you receive care from a provider who participates as an in-network provider from Sentara. When seeking medical care, if you use a health care provider who participates in the PPO network, your share of the cost of care is less. If you choose a non-PPO provider, covered expenses will be reimbursed as out-of-network, and your share of the cost will be more. You are encouraged to establish a relationship with a primary care physician. However, you may seek specifically care from any PPO-participating provider at any time without referral from the primary care physician.

In order to find a provider in the Sentara Network, you will need to first register. to register, log on to www.sentara.com from any computer with Internet access. on the homepage, enter your personal information as indicated. You will also need to create your own personal username and password in order to access your data. If you have difficulties with the registration, contact Sentara directly at 1-800-736-8272. Monday-Friday, 8AM-6PM EST.

For more details on this plan, please reference to detail Summary Plan Description for Sentara..

HSA ($3,300) and HSA ($2,500) Medical Plan

Health Savings Account (HSA) plans are consumer driven healthcare plans (CDHP). There are no co-pays in these plans. You must satisfy a deductible for most services before benefits are paid. All preventative care services are covered before deductible.

Benefits Of Health Savings Accounts

Health Savings Accounts (HSA) allows you to set aside pre-tax dollars to pay for care when you need it, now or in the future. You can use your HSA funds to pay for things such as; hospital visits, prescriptions drugs, co-pays, and more. A list of approved HSA qualified expenses can be found on the Employee Navigator site, as well as through Sentara’s site.

- You are setting aside money with pre-tax dollars.

- Your funds will roll-over year to year.

- Your funds stay with you; even if you change jobs, change plans, or retire.

- The money you put into an HSA, any interest you earn, and even the money you take out to pay for qualified expenses, is all

tax-free. - You can contribute up to $4,300 for an individual and 8,550 for a family.

- If you are 55 or older, you can contribute an extra $1,000 a year.

- EverGRO FS will provide an employer contribution towards an employee’s HSA account, based on the plan and tier enrollment

(see details below).

How Does An HSA Work

You must enroll in one of the HSA medical plans to be eligible to enroll/participate in an HSA. Once you select one of the HSA medical plans, through enrollment, you can select the amount you would like to place into your HSA for the calendar year, which will then be payroll deducted based on your biweekly pay periods.

The HSAs will be set-up as a spending account with a bank chosen by Anthem’s HSA Partner. Debit cards are issued to each HSA account holder which can then be used at doctor’s offices or pharmacies, dentists, eye doctors, etc., to pay for additional costs. The money comes directly out of the HSA account. Keep in mind, available funds are those that have been deposited based on payroll deductions (and the amount provided by EverGRO FS).

See included forms at the end of this benefit guide that highlight HSA eligible expenses.

Health Savings Account Employer Contributions

EverGRO FS will be providing an employer contribution to all employees who select to enroll in an eligible Health Savings Account (HSA) based on the plan and the tier of enrollment. For those employee’s enrolling during Open Enrollment, the amounts will be provided in full at the beginning of the calendar year.

For new employees, the employer contribution will be pro-rated based upon their eligibility benefit start date.

Employer Contributions

| HSA ($2500) | HSA ($2500) | |

| Employee Only | $700 | $900 |

| Employee & Spouse | $900 | $1,100 |

| Employee & Child | $900 | $1,100 |

| Employee & Children | $1,000 | $1,400 |

| Family | $1,200 | $1,600 |

Medical Premiums & Details

| Biweekly Premiums |

Sentara POS ($1,000) |

Sentara POS HSA ($2,500) Non-Embedded |

Sentara POS HSA ($3,300) Embedded |

| Employee Only | $116.47 | $18.71 | $19.38 |

| Employee + Spouse | $324.09 | $94.73 | $98.10 |

| Employee + Child | $156.46 | $21.94 | $22.72 |

| Employee + Children | $245.53 | $57.87 | $59.94 |

| Family | $412.83 | $112.12 | $116.11 |

*AD=After Deductible

| Biweekly Premiums |

Sentara POS ($1,000) |

Sentara POS HSA ($2,500) Non-Embedded |

Sentara POS HSA ($3,300) Embedded |

| Calendar Year Deductible | $1,000/$2,000 | $2,500/$5,000 | $3,300/$6,600 |

| Annual Out-Of-Pocket Max. Individual/Family (including deductible) |

$4,500/$9,000 | $5,000/$10,000 | $5,000/$10,000 |

| Co-Insurance | 0% AD | 20% AD | 0% AD |

| General/Family Practice Internist/Pediatrician |

$20 Copay | 20% AD | 0% AD |

| Specialist | $40 Copay | 20% AD | 0% AD |

| Inpatient Care Hospital Care for Illness, Injury, Maternity (Mother) & Surgery, Mental Health, Substance Abuse |

$500 Copay | 20% AD | 0% AD |

| Urgent Care | $40 Copay | 20% AD | 0% AD |

| Emergency | $350 Copay | 30% AD | 20% AD |

| Preventative Care Well Child Care & Adult Routing Well Care, Women’s & Men’s Preventative Service |

No Charge | No Charge | No Charge |

| Family | $412.83 | $112.12 | $116.11 |

Prescription Drug Coverage

| Sentara POS ($1,000) |

Sentara POS HSA ($2,500) Non-Embedded |

Sentara POS HSA ($3,300) Embedded |

|

| Tier 1 | $15 Co-Pay Retail Deductible does not apply |

$10 Co-Pay Retail After deductible* |

$10 Co-Pay Retail After deductible* |

| Tier 2 | $40 Co-Pay Retail Deductible does not apply |

$40 Co-Pay Retail After deductible* |

$40 Co-Pay Retail After deductible* |

| Tier 3 | $75 Co-Pay Retail Deductible does not apply |

$60 Co-Pay Retail After deductible* |

$60 Co-Pay Retail After deductible* |

| Tier 4 - Up to Max $300* | 20% up to $300 | 20% AD up to max $300 *Certain preventative drugs are covered before deductible. Reference Sentara plan details. |

20% AD up to max $300 *Certain preventative drugs are covered before deductible. Reference Sentara plan details. |

Retail Pharmacy

Your Sentara medical identification card is all you need to get full benefits at any participating retail pharmacy for your outpatient prescription drugs. You may receive up to a 30-day supply of medication for short-term use (such as antibiotics) or maintenance medications (such as high blood pressure or high cholesterol) from a participating retail pharmacy.

To find participating pharmacies near you, visit Sentarahealthplans.com and go to “Members”, and then click on “Find Doctors/Drugs/Facilities.”

For detailed information on the deductible and co-pays for each medical/prescription plan, please reference the Sentara guide.

Prescription Drug Classification

Your 4-tier prescription drug plan gives you access to most drugs in covered classes within the confines of your plan’s benefit design. Under your plan, covered brand name and generic drugs are categorized into 4 specific tiers, and each tier is assigned a co-pay level:

First Tier

This tier will contain low-cost or preferred medications and may include generic and single source brand drugs.

Second Tier

This tier contains preferred medications that generally are moderate in cost and may include generic and single-source and

multi-source brand drugs.

Third Tier

This tier contains non-preferred or high-cost medications and may include generic and single-source or multi-source brand

drugs.

Fourth Tier

This tier contains specialty Medications.

A generic drug is the chemical equivalent of brand-name drug. Generic drugs have the same ingredients as their brand-name equivalents and must meet the same standards for safety, strength, and effectiveness. Generic drugs will always be dispensed. If the physician or you request the brand name drug, you will pay the costs associated with the co-pay listed above for that tier medication; there are no deductibles in our prescription drug programs.

90-Day Supply

If you order a 90-day supply of medication, your costs would be Retail x 2.5 (as listed above).

NOTE: If you are currently filling a maintenance medication with a 30-day supply at a retail pharmacy, you are allowed two refills at your current pharmacy. After that, you will need to switch to a 90-day supply at a preferred retail pharmacy or through the mail order delivery method. You can locate a preferred retail pharmacy to fill a 90-day supply or fill your prescription through order by contacting Sentara.

Prescription Drug Coverage

Please note that when you are enrolled in a Sentara $1,000 (low deductible) Plan, prescription drug coverage may be different from the Sentara POS Health Savings Account (HSAs). The costs associated with medications you may take on a frequent basis, sometimes referred to as “maintenance” medication, may differ based on the HSA plans.

To help understand the potential costs associated with any maintenance medications, please contact your HR representative or our partners at Blue Ridge Insurance.

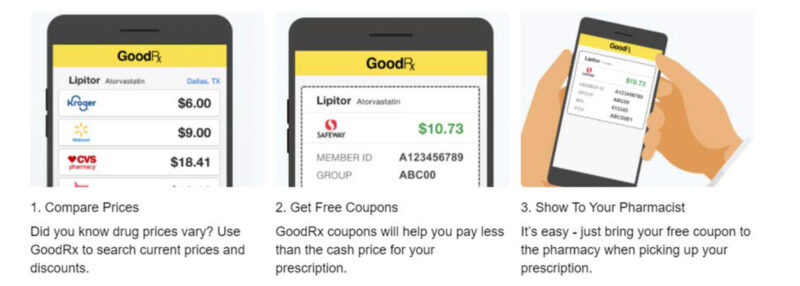

Good Rx - Discounts on Prescription Drugs

To help save on costs associated with prescription drugs, that may extend beyond the co-pays outlined, you can leverage additional discounts through Good Rx. Purchased prescriptions through GoodRx will not be counted towards deductibles.

This application can be downloaded on any smart phone by visiting the Apple Store or Google Play. You can also visit their website at, GoodRx.com to sign up for their services or simply vary the lowest prices and locations where you can access

any type of prescription.

Anthem Dental—Low Plan

| Biweekly Premiums | Low |

| Employee Only | $3.43 |

| Employee + Spouse | $6.87 |

| Employee + Child(ren) | $6.87 |

| Family | $9.73 |

Low Plan

| Deductibles | In-Network | Out-of-Network |

| Annual Deductible | $50.00 | $50.00 |

| Family Deductible Multiple | 3x Individual | 3x Individual |

| Deductible Waves—Diag/Prev | Yes | Yes |

| Deductible Waived—Orthodontics | Not Applicable | Not Applicable |

| Cost-Shares | In-Network | Out-of-Network |

| Diagnostic & Preventative | 100% Coinsurance | 100% Coinsurance |

| Basic Restorative | 80% Coinsurance | 80% Coinsurance |

| Non Surgical Endodontics | Not Covered | Not Covered |

| Surgical Endodontics | Not Covered | Not Covered |

| Non Surgical Periodontics | 80% Coinsurance | 80% Coinsurance |

| Surgical Periodontics | Not Covered | Not Covered |

| Simple Oral Surgery | Not Covered | Not Covered |

| Major Restorative | Not Covered | Not Covered |

| Prosthetics | Not Covered | Not Covered |

| Prosthetic Repairs & Adjustments | Not Covered | Not Covered |

| Orthodontics | Not Covered | Not Covered |

| Orthodontic Covers | None | None |

| Maximums | In-Network | Out-of-Network |

| Annual Maximum | $750.00 | $750.00 |

| Annual Maximum Carryover/Carry in | No/No | No/No |

| Out of Pocket Maximum Individual/Family | Not Applicable | Not Applicable |

Anthem Dental—High Plan

| Biweekly Premiums | High |

| Employee Only | $6.76 |

| Employee + Spouse | $13.59 |

| Employee + Child(ren) | $19.02 |

| Family | $25.63 |

High Plan

| Deductibles | In-Network | Out-of-Network |

| Annual Deductible | $50.00 | $50.00 |

| Family Deductible Multiple | 3x Individual | 3x Individual |

| Deductible Waves—Diag/Prev | Yes | Yes |

| Deductible Waived—Orthodontics | Yes | Yes |

| Cost-Shares | In-Network | Out-of-Network |

| Diagnostic & Preventative | 100% Coinsurance | 100% Coinsurance |

| Basic Restorative | 80% Coinsurance | 80% Coinsurance |

| Non Surgical Endodontics | 50% Coinsurance | 50% Coinsurance |

| Surgical Endodontics | 50% Coinsurance | 50% Coinsurance |

| Non Surgical Periodontics | 80% Coinsurance | 80% Coinsurance |

| Surgical Periodontics | 50% Coinsurance | 50% Coinsurance |

| Simple Oral Surgery | 50% Coinsurance | 50% Coinsurance |

| Major Restorative | 50% Coinsurance | 50% Coinsurance |

| Prosthetics | 50% Coinsurance | 50% Coinsurance |

| Prosthetic Repairs & Adjustments | 50% Coinsurance | 50% Coinsurance |

| Orthodontics | 50% Coinsurance | 50% Coinsurance |

| Orthodontic Covers | Dependent Children Only | Dependent Children Only |

| Maximums | In-Network | Out-of-Network |

| Annual Maximum | $1,500.00 | $1,500.00 |

| Annual Maximum Carryover/Carry in | Yes/Yes | Yes/Yes |

| Out of Pocket Maximum Individual/Family | Not Applicable | Not Applicable |

| Lifetime Orthodontic Maximum | $2,000.00 | $2,000.00 |

DENTAL DETAILS & FINDING A DENTISYWhen you receive care from an out-of-network provider, benefits will be based on the 95th percentile of the usual customary charges. Therefore, you would be responsible for paying the difference of the out-of-pocket expense and what Anthem found to be as the 95th percentile of that costs in-network.

To find a dentist in-network, visit Anthem.com/provider/dental. If your favorite dentist is not in-network please let HR or Blue Ridge Insurance now of this and they can look into the possibility of that provider joining the network.

Vision Plans

| Biweekly Premiums |

Sentara VIP® Savings Pass ($1,000) |

Anthem Standard (Materials Only) |

Anthem Premium (Full Service) |

| Employee Only | No Cost Must be enrolled in a medical plan |

$2.17 | $2.52 |

| Employee + Spouse | No Cost Must be enrolled in a medical plan |

$4.49 | $5.22 |

| Employee + Child(ren) | No Cost Must be enrolled in a medical plan |

$4.98 | $5.79 |

| Family | No Cost Must be enrolled in a medical plan |

$7.86 | $9.15 |

Anthem - Standard (Materials Only) VP

Plan Details

Your Anthem Standard plan provides coverage for various eye care material needs only, shown below. Members may choose to upgrade their new eyeglass lenses at a discounted cost. Cost shown are after any applicable eyeglass lens copayment. Please refer to the Anthem guide for more details.

| Progressive Lenses - Standard | $50 | Transitions Lenses (Adults) | $75 |

| Progressive Lenses - Tier 1 | $85 | Transitions & Polycarbonate Lenses (Pediatrics) | $0 |

| Progressive Lenses - Tier 2 | $95 | Standard Polycarbonate Lenses (Adults) | $40 |

| Progressive Lenses - Tier 3 | $110 | UV Coating | $15 |

| Progressive Lenses - Tier 4 | $175 | Tint (Solid & Gradient) | $15 |

| Anti-Reflective Lenses - Standard | $45 | Other Lens Upgrades & Add-Ons | 20% Off Retail |

| Anti-Reflective Coating - Tier 1 | $57 | Add. Supplies of Conventional Contact Lenses After Benefits Have Been Used |

15% Off Retail |

| After Benefits Have Been Used | |||

| Anti-Reflective Coating - Tier 2 | $68 | Additional Complete Pairs of Eyeglasses | 40% Off Retail |

| Anti-Reflective Coating - Tier 3 | $85 | Eyeglass Materials Purchased Separately | 20% Off Retail |

| 20% Off | Other Items Including Non-Prescription | 20% Off Retail | |

| Remaining Balance |

Sunglasses, Eyewear Accessories such As Lens | ||

| Cleaning Supplies, Contact Lens Solutions, Eyeglass Cases, etc. |

Elective Contact Lenses (Non-Disposable): Contact lens allowance will only be applied toward the first purchase of contacts made during a benefit period. Any unused amount remaining cannot be used for subsequent purchases in the same benefit period, nor can any unused amount be carried over to the following benefit period

15% Off Remaining Balance

Additional Discounts & Benefits from Sentara

See the links in the Table of Contents

Flexible Spending Account (FSA)

Healthcare Flexible Spending Account (FSA)

A Health Care FSA supplements your health care coverage by helping to pay for certain expenses, with tax-free dollars, not reimbursed by other medical, dental, or vision plans. You can use this account for the types of healthcare expenses you would qualify as itemized deductions on your income tax return. In general, most health care

expenses not covered by an insurance plan are eligible for reimbursement through this account.

*For more information on any type of Flexible Spending Account please contact your human resources department.*

How the Account Works

The Maximum amount you can contribute to your Health Care FSA is $3,200 per calendar year. The minimum amount you must contribute to enroll is $260 per calendar year. The amount you decide to put into the account will be deposited through pre-tax, payroll deductions.

You may seek reimbursement any time during the year when you have incurred eligible expenses. Reimbursements are handled either at the point of sale through a debit card issued by the administrator or by submitting a claim after the expense has been incurred.

If a claim is submitted, a check will be mailed directly to you, along with an explanation of payment, or you can choose to have the payment direct deposited into your bank account. Detailed information regarding the debit card and claim submission will be sent to you once enrolled in the plan.

Use It or Lose It

Federal regulations allow a two and a half “grace period” following the end of the plan year to incur expenses. This means you can incur eligible expenses from 1/1/25 through 3/15/26 to qualify for reimbursement from the previous year’s FSA. You then have until 4/30/26 to request reimbursement from your account for those expenses. After that, any remaining balance is forfeited. In other words, you must use it or lose it!

Dependent Care Flexible Spending Account (FSA)

The Dependent Care FSA allows you to set aside pre-tax money to reimburse yourself throughout the year for eligible dependent care expenses. If you are married, your spouse must also be employed or a full-time student for at least 5 months during the year, or be disabled and unable to provide his or her own care.

Reimbursable dependent care expenses must be for children under the age of 13, a disabled spouse, or disabled dependent of any age.

How the Account Works

The maximum amount you can contribute to your Dependent Care FSA is $5,000 per calendar year. The minimum amount you must contribute to enroll is $260 per calendar year. The amount you decide to put into the account will be deposited through pre-tax, payroll deductions.

You may seek reimbursement any time during the year when you have incurred eligible expenses. Reimbursements are handled by submitting a claim after the expense has been incurred and funds are available in your account.

When a claim is approved, a check will be mailed directly to you, along with an explanation of payment, or you can choose to have the payment direct deposited into your bank account. Detailed information regarding claim submission will be sent to you once enrolled in the plan.

Eligible Expenses

In order to be an eligible expense for Dependent Care FSA, the care must be provided by a licensed individual, nursery school, or daycare center.

Use It or Lose It

Federal regulations allow a two and a half “grace period” following the end of the plan year to incur expenses. This means you can incur eligible expenses from 1/1/25 through 3/5/26 to qualify for reimbursement from the previous year’s FSA. You then have until 4/30/26 to request reimbursement from your account for those expenses. After that, any remaining balance is forfeited. In other words, you must use it or lose it!

Limited Purpose Flexible Spending Account (LPSFA)

The LPFSA is much like a typical traditional Health Care Flexible Spending Account. However, under a LPFSA, eligible expenses are limited to qualifying dental and vision expenses for you, your spouse and your eligible dependents. Also, you must be enrolled in the HSA plan to be eligible to enroll in a LPFSA.

How the Account Works

- Pre-tax payroll contributions, resulting in income tax settings.

- Maximum annual limit is $3,200

- Reimburses primarily Dental and Vision expenses

- Dental card

- “Use it or Lose it!”

For more information on FSA’s, contact your human resources department; (540) 672-2977 ext. 229

Company Paid & Voluntary Benefits

Through our partnership with Mutual of Omaha the following benefits will be either provided to each full-time eligible employee or offered as a voluntary benefit. In addition, there are other offerings Mutual of Omaha provides its participants including; Will Preparation, Employee Assistance Program and Travel Assistance.

Group Life Insurance Plans

EverGRO FS Life Insurance Plans are issued through Mutual of Omaha. EverGRO FS pays for Basic life insurance coverage for eligible employees and their eligible dependents. Employees have the option of purchasing additional coverage for themselves and for their dependents with after-tax dollars.

BASIC LIFE INSURANCE AND AD&D INSURANCE

EverGRO FS provides life insurance coverage to the employee’s beneficiary in the event of your death while you are covered under the plan. The amount of your life insurance coverage will be 1x employee’s salary, up to $150,000 and will also include a $10,000 coverage for all eligible dependents. In addition, EverGRO FS will provide up to 1x employee’s salary for AD&D.

SUPPLEMENTAL LIFE INSURANCE

Voluntary life is also available up to 5x annual salary with a guaranteed issue of up to $100,000. For current employees, pay is defined as their base annual pay, as the last pay period in December, rounded up to the nearest $1,000. For new hires, base salary is the base pay at the time they’re classified as a regular full-time employee, rounded up to the nearest $1,000.

EVIDENCE OF INSURABILITY

If requesting coverage that requires medical underwriting, you will be required to provide Evidence of Insurability to the carrier.

ACCELERATED DEATH BENEFIT

The life insurance plan has an accelerated death benefit provision. The accelerated death benefit provides for the early payment of up to 80% of life insurance coverage (up to $500,000) in the event of terminal illness.

BENEFICIARY DESIGNATION

To designate a life insurance beneficiary(ies), employees must enter them online when enrolling in their benefits. Beneficiaries can be changed online at any time during the year.

ADDITIONAL SPOUSE LIFE

Additional Spouse Life coverage can be purchased with a minimum benefit of $5,000, in $5,000 increments and a maximum benefit up to $150,000 with a guaranteed issue amount of $25,000.

ADDITIONAL CHILD LIFE

Additional Child Life coverage can be purchased with a minimum benefit of $2,000, in $1,000 increments and a maximum benefit up to $10,000 with a guaranteed issue amount of $10,000.

NOTE: For both Spouse and Childe Life - In the situations where both husband and wife are employees, a spouse cannot be a dependent on a spouse life and child life can only be elected by one employee.

Disability

Short-Term Disability

The short-term disability plan is administered through Mutual of Omaha. Employees will need to contact their human resources department to initiate a claim or they can directly initiate a claim through Mutual of Omaha by submitting a request claim form. Short-term disability benefits provide continuing income if an employee were

absent from work due to a qualifying illness or injury that occurred outside of the working environment. This benefit is provided at no cost to employees.

For each calendar year employees are eligible for a maximum of up to 12 weeks of STD. Employees will have a eight-day waiting period from the day they begin their leave of absence, until when the STD benefit takes effect. During that waiting period, employees will need to use any earned and unused PTO days or else it will be unpaid.

During the STD period, employees are eligible to be paid a primary weekly benefit of 60% of their earnings up to $1,400.

*There are limitations and variances based on exclusions and other details. Please reference the Mutual of Omaha’s guide for details.

Long-Term Disability

Employees are eligible for long-term disability (LTD) benefits after they have completed the elimination period, which is the greater of the short-term disability maximum benefit period or 90 days. The LTD benefits is 60% of pay, with a maximum monthly benefit of $7,000. The occupation period will be up to 2 years. This benefit is provided at no cost to employees.

*There are limitations and variances based on exclusions and other details. Please reference the Mutual of Omaha’s guide for details.*

Additional Voluntary Benefits

Critical Illness

The Critical Illness plan is administered by Mutual of Omaha and is a voluntary benefit for both the employee and their spouse in the case they are accidentally injured off the job. This coverage pays an up-front, lump-sum benefit for injuries received from an accident to use any way they choose, regardless of other insurance they have or actual expenses incurred.

Some examples of critical illnesses include, but not limited to the following - heart attack, loss of hearing, invasive cancer, stroke, major organ failure, skin cancer and several childhood conditions.

*There are limitations and variances based on exclusions and other details. Please reference the Mutual of Omaha’s guide for details.

Accident

Mutual of Omaha also administers accident insurance. Accident insurance helps employees maintain financial wellness when it comes to unexpected injuries by providing support to help cover expenses associated with that injury. The Accident benefit pays an up-front, lump-sum based on covered injuries received. It’s not dependent on services, tests or treatments, so employees can get paid right away with less paperwork.

Some examples of injuries covered include - burn, coma, concussion, dental injury, eye injury, dislocation, fracture, internal injury, disc, knee cartilage, tendon, ligament or rotator cuff injury, and more.

*There are limitations and variances based on exclusions and other details. Please reference the Mutual of Omaha’s guide for details.

Will Preparation Services

Click here to download the PDF Brochure

Employee Assistance Program (EAP)

Click here to download the PDF Brochure

Paid Time Off

EverGRO FS provides full-time eligible employees Paid Time Off (PTO) to be used for reasons, including but not limited to, personal days, vacation, and sick time. We encourage our employees to take time away from work to reenergize!

PTO is accrued per pay period based on the accrual rates listed. Employees cannot take time off without using accrued PTO (i.e. PTO is not allowed to fall into the negative). Any exception to this policy must be reviewed and approved by the General Manager and HR.

PTO continues to accrue until it reaches the maximum, 256 hours. Accumulated PTO may not exceed 256 hours (32 days). Once an employee’s PTO reaches the maximum rate, no additional PTO can be accrued until the balance falls below 256 hours. PTO does not accrue, however, during an employee’s leave of absence (STD/LTD/FMLA, etc.)

Upon separation of employment, employees will be paid for their unused and earned PTO, up to a maximum payout of 120 hours. PTO cannot be used to extend an employee’s separation date nor their two weeks’ notice.

PTO requests must be submitted through Paylocity and approved by the employee’s supervisor. A minimum of 48 hours is requested when submitting one or more days off, with at least one month notice when requesting one or more weeks of PTO.

PTO Allocation

| Length of Service | Full-Time Accrual Rate |

| 0-2 Years | 4.30 Hours/Pay Period |

| 3-5 Years | 5.23 Hours/Pay Period |

| 6-10 Years | 6.15 Hours/Pay Period |

| 11-15 Years | 7.07 Hours/Pay Period |

| 16-19 Years | 8.00 Hours/Pay Period |

| 20+ Years | 9.23 Hours/Pay Period |

Additional Time Off Benefits

Full time employees are also eligible for additional time off (which may be paid or unpaid) and include -

- Bereavement

- Jury Duty

- Volunteer Service

- Floating Holidays

- Holiday Banked Hours

- Voting Time

- FMLA

- Maternity / Paternity Paid Time

For more details on other paid time off please contact your HR department at (540) 672-2977, ext. 229.

Company Holiday Schedule

EverGRO FS observes and provides time off with pay for the following holidays:

- New Years’ Day

- Memorial Day

- Independence Day

- Labor Day

- Thanksgiving Day

- Christmas Day

In addition to paid holidays, the company will provide full-time employees two (2) Floating Holidays each calendar year. Part-time employee are not eligible for floating holidays and will receive the company holidays off as unpaid. Floating Holidays are to be requested following the standard PTO practices and if they are not used by December 31st, they will be lost and starting on January 1st, the employee will be re-issued 16 hours of Floating Holiday to be used in that calendar year. New hires will receive Floating Holidays and Volunteer Time on a pro-rated basis.

Company observed holidays and floating holidays will be counted as 8-hours or regular straight-time and are not used towards overtime calculations. If an employee works on a holiday they will receive time-and-a-half pay for the hours they work and they will be given another day off, known as “holiday bank” with pay in its place per the approvals of the department manager. To be eligible for a paid company holiday, the full-time employee must be in a paid or approved status their scheduled day before and after the holiday.

Employee Perks

EverGRO FS also provides additional employee benefits to assist with your growth and development in your professional and personal life. Below are some additional benefits.

Employee Hardship Payroll Advances

EverGRO FS recognizes that employee’s may experience unexpected, urgent financial strains throughout the year. In the case of these unfortunate circumstances, EverGRO FS has implemented a ‘Employee Hardship Payroll Advance Policy’ that will provide an employee the opportunity to request a payroll advance up to a fixed amount one time per calendar year, based on approvals by the General Manager and HR.

The payroll advance amounts will be based on leveraging an employee’s current earned/unused PTO balance as collateral towards the payroll advance amount. In addition, the employee must review and agree to the terms and conditions of repaying the advance through payroll deductions. Once the payroll advance is repaid, the employee’s PTO that was leveraged will be restored. Only eligible for full-time employees.

Tuition / Learning Reimbursement

As employee’s look to grow their careers with EverGRO FS, we support the opportunity to help reimburse them for enrolling and attending college/continuing education courses that are related to their position and the Co-op’s mission, up to a fixed amount per year. Approvals must be obtained prior to completing and enrolling in the courses. Reimbursement for course materials may also be considered. Only eligible for full-time employees.

EverGRO FS will also consider reimbursements for additional outside trainings, seminars, courses, conferences etc. Approvals must be obtained prior to enrolling in the courses or attending any outside training from the employee’s direct supervisor.

Employee Discounts

All employees, both full-time and part-time are eligible for employee discounts on most retail products and services. The discounts are typically 5% over costs and must be purchased at one of our stores. Employee’s immediate family members, which includes spouse and children, are also eligible for the employee discounts on retail purchases.

Special pricing for fuel, propane and other items are available. Please consult the Division Directors related to discount pricing on Energy or Agronomy related products and services.

Discounts must be for personal use only and may not be associated with an outside personal business endeavor.

Uniform Services / Safety Shoes

Based on the employee’s role, both full-time and part-time employees will be provided uniforms. This could include shirts, high visibility attire, pants, etc. For office positions, an annual amount is allocated to each employee to purchase EverGRO FS logoed clothing through their business account vendor online.

For positions requiring safety-toed shoes, the Co-op will pay, up to a fixed amount, to help cover costs. For more details or questions regarding eligibility or participation in any of the policies referenced, please see HR, your supervisor or your Division Director.

Fitness / Health Reimbursement

EverGRO FS wants to support your journey to a healthy and happy lifestyle by reimbursing you (and your spose) for eligible expenses related to gym memberships, nutrition coaching, personal training, fitness courses and more. This reimbursement will be paid out twice a year by submitting EverGRO’s application with necessary

receipts/proof of payments.

Retirement Savings Plan (RSP)

The EverGRO FS Retirement Savings Plan (RSP) is your personal retirement plan. It provides you with the opportunity to save with pre-tax dollars and receive employer matching dollars at the same time. You can also contribute post-tax, but those contributions are not

matched.

Sponsored by EverGRO FS, it is an easy and convenient way for you to save for your future retirement needs through payroll deduction.

Your Contributions

You must actively call (888) 708-6988 or enroll online at www.millimanbenefits.com to begin your 401k contributions. Your employee pre-tax contributions can be from 0%-50% of compensation (IRS deferral limits apply, which for 2025 are $23,500 +plus catch-up of up to $7,500). You are eligible to begin participating in the 401k plan on the first day of the month following 90 days of

employment.

Employer Contributions

To help you save for your future, EverGRO FS will contribute 100% match on the first 4%. In addition, EverGRO FS will contribute 50% on the next 2%. Therefore, if you elect to contribute 6%, EverGRO FS will be matching your contributions $1 for $1 on 5%.

Vesting

You will be vested immediately in your contributions and the matching contributions from the Coop.

Retirement Plan Carrier

The Milliman Group will be the carrier of EverGRO FS’ 401k retirement plan. For any questions related to the 401K Plan, please contact a representative from The Milliman Group or the HR department.

Health Savings Account Eligible Expenses)

HSA Examples of Eligible Expenses

Your EverGRO FS health savings account (HSA) may reimburse:

- Qualified medical expenses incurred by the account beneficiary and his or her spouse and dependents

- COBRA premiums

- Health insurance premiums while receiving unemployment benefits

- Qualified long-term care premiums*

- Any health insurance premiums paid, other than for a Medicare supplemental policy, by individuals age 65 or older; and

- Certain personal protective equipment (PPE) - such as masks, hand sanitizer and sanitizing wipes - used for the primary purpose of preventing the spread of COVID-19; and

- Effective Jan. 1, 2020, qualifying over-the-counter (OTC) drugs, along with menstrual care products, are also treated as qualified medical expenses.

Distributions made from an HSA to reimburse the account beneficiary for eligible expenses are excluded from gross income.

Qualified Medical Expenses

The Internal Revenue Service (IRS) defines qualified medical care expenses as amounts paid for the diagnosis, cure or treatment of a disease, ad for treatments affecting any part or function of the body. The expenses must be primarily to alleviate a physical or mental defect or illness.

The products and services listed below are examples of medical eligible for payment under your HSA, when such services are not covered by your high-deductible health plan. To be an expense for medical care, the expense has to be primarily for the prevention or alleviation of a physical or metal defect or illness.

The list is not all-inclusive; additional expenses may qualify, and the items listed below are subject to change in accordance with IRS regulations. For more information or clarification on individual list items, refer to Publication 502 or consult a tax professional.

- Abortion

- Acupuncture

- Alcoholism

- Ambulance

- Annual physical examination

- Artificial limb

- Artificial teeth

- Bandages

- Birth control pills

- Body scan

- Braille books and magazines

- Breast pumps and supplies

- Breast reconstruction surgery

- Capital expenses

- Car Chiropractor

- Christian Science practitioner

- Contact lenses

- Crutches

- Dental treatment

- Diagnostic devices

- Disabled dependent care expenses

- Drug addiction

- Eye Exam

- Eyeglasses

- Eye surgery

- Fertility enhancement

- Founder’s fee

- Guide dog or other service animal

- Health institute

- Health maintenance organization (HMO)

- Hearing aids

- Home care

- Home improvements

- Hospital services

- Insurance premiums

- Laboratory fees

- Lactation expense

- Lead-based paint removal

- Learning disability

- Legal fees

- Lifetime care - advance payments

- Lodging

- Long-term care

- Meals

- Medical conferences

- Medical information plan

- Medicines

- Nursing home

- Nursing services

- Operations

- Optometrist

- Organ donors

- Osteopath

- Oxygen

- PPE used for the primary purpose of

preventing the spread of COVID-19, such as:

-Masks

-Hand sanitizer

-Sanitizing wipes - Physical Examination

- Pregnancy test kit

- Premium tax credit

- Prescribed weight-loss programs

- Prescription drugs

- Prosthesis

- Psychiatric care

- Psychoanalysis

- Special education

- Special home for intellectually an developmentally disabled

- Sterilization

- Stop-smoking programs

- Surgery

- Telephone

- Television

- Therapy

- Transplants

- Transportation

- Trips

- Tuition

- Vasectomy

- Vision correction surgery

- Wheelchair

- Wig

- X-ray

Source: www.irs.gov

Plans that do not allow reimbursement of all eligible medical expenses as defined by the IRS and Department of Treasury must customized this article prior to use.

*For purposes of reimbursement of qualified long-term care premiums from an HSA, reimbursement in excess of the amount which may be deducted on an individual’s personal tax return is not an eligible expense. IRS 213(D)(10) establishes the tax deduction allowed for qualified long-term care premiums on individual tax returns. If the HSA reimburses long-terms care premiums for an amount greater than set forth in IRC 213(d)(10), the amount greater than allowed is included in the account holder’s taxable income and is subject to a 20 percent penalty.

Table Of Contents

(Click links to advance to each section)

Welcome Message

Benefit Options

Medical Plans Information

Medical Plans Summaries

Health Savings Account Employer Contributions

Medical Premiums & Details

Prescription Drug Coverage

Anthem Dental Low Plan

Anthem Dental High Plan

Vision Plans

Sentara Additional Benefits & Programs

(PDF Downloads)

Covered Preventative Care

VSP Vision Benefit - Employer Savings Pass

Sentara Mobile Application

MD Live Benefit

Treatment Cost Calculator

Sentara Well-Being Rewards Program

Sentara Diabetes Treatment Program

Sentara Husk Wellness-Fitness Program

Emergency Travel Assistance

MD Therapist Live Benefit

More Employee Health Benefits

Flexible Spending Accounts (FSA)

Mutual of Omaha Benefits & Programs

Group Life w/ AD&D and Voluntary Life

Short-Term & Long-Term Disability

Critical Illness & Accidental Insurance

Mutual of Omaha Brochure

(PDF Downloads)

Will Preparation

Employee Assistance Program

Additional Employee Perks

Retirement Savings Plan

Employee Perks

Paid Time Off (PTO)

Health Savings Account Eligible Expenses